The 1980s was a time of recovery, for markets in particular and capitalism generally.

In contrast, the 1970s for the UK had been a time of huge turbulence, politically, economically, and socially – there were painful adjustments for many older industries and the communities which relied on them (which continued some way into the 1980s).

That the problems of the UK were more deep-seated than elsewhere in the world was reflected by the markets. For example, the UK stock market fell by 72% from peak to trough in 1972-74, while US prices fell by only 48%.

Then came a turnaround. By the 1980s the stock market was prepared to look beyond the continuing political turbulence, and social pain, and rose very sharply from 1982, celebrating a new era led by Ronald Reagan and Margaret Thatcher (who had been elected Prime Minister in 1979).

The big idea was that Governments were to shrink, and capitalism was to be allowed to flourish. Individualism and greed were good.

“This time next year we’ll be millionaires”

This was more than a Del Boy catch phrase – it was the mantra for a generation. And many of that generation went further, encouraged by laissez-faire Thatcherism, and embraced another Del Boy guide line:

“The government don’t give us nothing, so we don’t give the government nothing”

This new “can-do” culture was epitomised by the rise of the yuppie, with Filofax (you’ll have to Google that!) in one hand and the new-fangled mobile phone (the size of a house brick) in the other.

Shrinking the Government and popular capitalism combined to create an era of privatisations, selling off publicly-owned assets. In 1984, amidst massive publicity, British Telecom was sold off. Two-fifths went to the general public, mostly novice investors, and on 20th November 1984 there were 2.1 million new budding capitalists enjoying an investment which doubled in value on the first day.

“If you see Sid, tell him”

As well as Del Boy, other populist characters were born. Say “hello” to Sid. By 1986 it was the turn of British Gas to be privatised, the most ambitious to date. To encourage participation the slogan was invented: “If you see Sid, tell him”. Four million “Sids” applied for shares in British Gas, 1.5m received an allocation, and many sold within the first few days for another handsome profit.

In 1985 the new FTSE 100 index was up 14%, and up 19% in 1986.

Such was the background to 1987.

How could capitalism not be popular if you were going to give money away?

A new generation of individual investors were enjoying regular windfalls of apparently free money. Importantly, they were also increasingly confident as consumers. This growing confidence spread through the board rooms of the UK.

There were plenty of corporate predators, from Hanson to Polly Peck. Competition for big fish such as Distillers and Imperial Group ensured opening bids went much higher before these contests were settled.

Animal spirits abounded, a necessary ingredient for any budding mania worthy of the name.

Confidence in the US was also booming. US companies were issuing vast amounts of debt to go on spending sprees. The amount of debt issued in 1986 was twice as much as 1985, and this trend was to continue in 1987. Very early into 1987 the Dow Jones hit new highs, and volume was huge.

PART 2:

1987, a rollercoaster for popular capitalism

The opening of 1987 was full of optimism. In the UK in particular economic growth was accelerating, productivity was continuing to improve, governments revenues were above estimate, and there was political stability as re-election of the Thatcher regime was assured. (This was all a far cry from 2017).

The UK stock market was cheap by international standards, and this was illustrated by the wave of foreign buying.

This confidence was also evident around the globe – the precise reasons varied from country to country, but the confidence was infectious.

The growing worry was the evolution of confidence in stock markets.

“It’s never too late to make a profit, you make money while sleeping.”

A quote from 1987? No. Possibly early 1929? No. It was 1637, Tulip Mania in Holland.

One mania is like another in terms of investor behaviour. This quote was as relevant as we entered 1987 as in 1637. The constant through the ages is ALWAYS human nature, and, in the case of an investment mania, over-confidence to the point of irrationality – more on that later.

In 1987 Dennehy Weller & Co was in its infancy, so we worked hard to fill the gap in our experience through a deeper knowledge of stock market history and, in particular, what could go wrong.

For us, the FT and the Investors Chronicle were constant mainstream sources of feedback. Bob Beckman was a regular purveyor of apocalyptic analysis (though his hair-do distracted us from taking him too seriously!), and Robert Prechter published regular Elliott Wave analysis to make you stop and think. In addition the Traded Options Newsletter was a weekly source of common sense insights on the UK stock market.

Ahead of “The Crash” it was surprising how much reference there was to the possibility of a crash.

As early as January 1987 the legendary student of 1929, John Kenneth Galbraith, said:

“The dynamics of speculation are remorselessly constant…

…those who suffer most will be those who regard current warnings with greatest contempt”

This quote reflected one of the early cracks in the edifice of the mania that was building. Another was the extraordinary corruption and fraud which was being uncovered many months before October.

“Insider trading” and “junk bonds” became household phrases, and prison sentences were being handed out like confetti in the US. In the UK the Guinness Affair was rumbling, though no one had yet rumbled Polly Peck and Asil Nadir.

Yet while all of this was going on, the UK stock market was up 19% at the end of the 1st quarter of 1987.

As we moved into April, criminal rings were uncovered operating midst the US stock market, trading drugs for insider information. Two undercover agents stated that cocaine is either used or accepted by 90% of the people on Wall Street.

Nonetheless the hype was never-ending. In May one flakey US company was promoted by an analyst on the basis that “You are buying a dream”. This sort of hype was commonplace, and investors were still buying into it.

Turning back to the UK stock market, after a Spring tumble, Margaret Thatcher was comfortably re-elected, following another “budget for equities”, and the UK stock market continued its frothy rise.

In the 2nd quarter of 1987 alone the FTSE 100 index was up another 15%.

As an aside, by July there was growing anxiety over inflation as the oil price hit $22. (what we wouldn’t give for that kind of anxiety now!) It had been under $10 within the previous year.

The UK stock market peaked for the year on 16th July, up 45% in just 7 months. (The Dow Jones would not hit its high for the year until 25th August, when it would be up 44%).

PART 3:

Summer 1987: Reasons to be cautious

As we moved into August, the UK stock market fell sharply over concerns that it would not be able to cope with a raft of huge rights issues. The FT ran with a “Fear of the Crash” headline on 1st August, albeit on the inside pages.

At a personal level, in August we completed the takeover of a small firm of investment advisers. This made us all the more sensitive to unfolding events. Nonetheless, markets began to recover again as we entered September.

At this manic stage the market is (and was) inherently unstable, and it is inevitable that the mania will be followed by panic – at least history was absolutely clear on this in our view.

The problem is that there is no way to know what might trigger that panic and when.

Myself and Linden Weller certainly recall feeling unsettled and cautious at that time in 1987. The words “instinct” and “gut feeling” come to mind when we reflect on how we felt at that time – there was no single overwhelming fact which was making us nervous. Interestingly a survey conducted by Robert Shiller, at the time of the Crash, also found many large traders and investors expressing the same rather vague sentiment.

Yet there were plenty of raw facts in the Summer of 1987 to engender caution beyond mere gut feeling:

British Gas and earlier privatisations created an atmosphere in which the general public believed investing was “free money”.

In May 1987 the stock market offer for Sock Shop was 53 times over-subscribed!

One incident which rang a loud bell of unreality was the takeover approach from an advertising agency (Saatchi and Saatchi) for a huge High Street bank (Midland, now HSBC in the UK).

Wages were going up at a healthy clip, but there was no sense this was eating into company profits (and thereby making shares less attractive).

Consumer spending boom was encouraged by the easy availability of credit, and consumers were not put off by double digit interest rates which would scare us rigid in 2017.

With interest rates at 10% deposit rates were juicy. But the public was more interested in the easy money of the stock market through a raft of privatisations and new issues.

The dividend yield on shares was 3%, but interest on gilts was nearer 10%. The ratio between these two had never been so great, and highlighted a VERY expensive market i.e. surely you would prefer a guaranteed return of 10% in preference to the uncertainty of the stock market?

House prices were booming, despite mortgage rates of 12% at best, and nearer 15% for some. Booming confidence overwhelmed any possible fear of not being able to meet sky-high mortgage repayments.

With only a moment of reflection this was a worrying mix.

Over in the US there were similar but not identical signs.

Paul Volcker was replaced as head of the Federal Reserve in August 1987. A significant part of confidence in the US economy and stock market was based on the key person charged with managing the economy – Volcker. From 1979 he kept rates very high (peaking at 14% in May 1981) to slay the inflation dragon, which fell from a peak of 11.3% in the 1970s to 3.6% by 1987. The latter allowed rates to begin falling, a key element in the growing confidence of the 1980s.

Volcker leaving, and being replaced by the relatively unknown Alan Greenspan, was clearly not helpful. There were also obvious imbalances – budget deficit, trade deficit, and low savings rate. Plus the weak dollar had been a global pre-occupation for much of 1987.

But none of these were sufficient either alone or combined to cause The Crash.

“Tensions were building” according to Manuel Johnson, vice chairman of the Federal Reserve under Volcker and Greenspan – he continued:

“the divergence between the pricing of bond and equity markets had been obvious for quite a while.”

It was expected that there would be a reaction – it was the magnitude which was “a total shock” he said, as we will see.

In 1986 there were rumblings about the dangers of the use of computers set up to quickly trade large numbers of shares, so-called program trading. This took two forms.

The first was portfolio insurance, where a computer model worked out how much to sell to limit losses when the stock market was falling. Typically the “selling” was done through the futures market rather than by selling individual shareholdings.

The second type of program trading was “index arbitrage”. This was designed to make profits by exploiting price discrepancies between the value of shares in a stock market index and the value of the equivalent futures contract.

Despite some concerns, there was no drive to understand these better, beyond a study which was commissioned in July 1987 by John Phelan, chairman of the New York stock exchange. His concerns were largely ignored because a lot of money was being made through these innovations – that feels like 2007/8, on which watch The Big Short.

Manuel Johnson says there were “concerns” over these financial innovations. But the truth is that even if they understood them technically, they did not fully understand the dangers. There was also a laissez-faire attitude, a bias against interference.

In January 1987 Galbraith saw a:

“commitment to seemingly imaginative, currently lucrative, and eventually disastrous innovation in financial structures”

Just as in 1929. And just as we saw in the years leading up to The Great Financial Crisis of 2008.

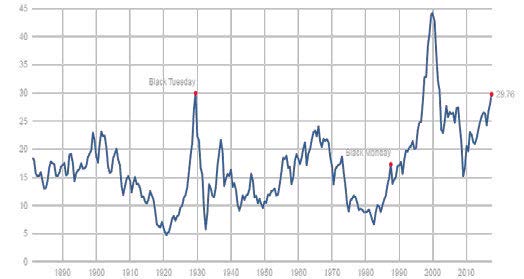

Valuations were not extreme (though John Phelan says they were “reasonably high”). That they were not extreme can be illustrated by a long term chart of a measure widely used today, the cyclically-adjusted price earnings ratio, CAPE. Looking at the CAPE chart (below) for the US stock market, Black Monday barely registers – though see how 2017 stands out.

Similarly on a simpler price earning s ratio, based on the current years earnings. This spiked up through 20 in Spring/Summer 1987, but it had been flirting with 20 for more than a decade from the early 1960s – so this was far from an overwhelming worry. This measure was somewhat lower in the UK.

Similarly on a simpler price earning s ratio, based on the current years earnings. This spiked up through 20 in Spring/Summer 1987, but it had been flirting with 20 for more than a decade from the early 1960s – so this was far from an overwhelming worry. This measure was somewhat lower in the UK.

But there was one clear warning, John Phelan again: “If you wanted to park your car in New York you got three stock tips from the attendant”. So no big valuation concern – but a very clear concern about investor behaviour, just as in the UK.

Rich history of bad behaviour

It was the behaviour of investors in particular which concerned us at the time. There was already a rich literature on stock market manias, from the 19th century work of Mackay to the recent classic of Charles Kindleberger, “Manias, Panics, and Crashes”.

What lies at the heart of a mania was captured more recently by Akerlof and Shiller. Extremes are caused by the inter-action of confidence, greed and fear, temptations, envy, resentment and illusions. And, in the case of a mania, they are held together by a good story, widely believed, which binds the crowd of investors more tightly together.

The story was very powerful.

The 1970s had been very tough, and the Thatcher government wanted everyone to believe in a better today and an even better future. It certainly didn’t stop with privatisation windfalls.

For example, the FT called the 1986 budget a “budget for equities” – income tax was cut, allowances raised, money supply target increased, interest rates cut.

To ensure the widest possible participation in this largesse the Government also introduced a “right to buy” for Council house tenants. Discounts were up to 50%, and 100% mortgages were guaranteed to be made available by the local council. More free money.

The fire was well and truly being stoked.

In the US too. The markets had already been reaching higher all-time highs in 1985 and 1986. Then in October 1986 President Reagan slashed the top rate of tax from 50% to 28%. There were now just two tax rates, and a raft of simplifications. From the day before the Tax Reform Act of 1986 was signed the stock market took off, and rose by over 50% in the next 10 months.

Before the worst crashes of the 20th century (such as 1907,1929,1987, and 2000) the market was already performing well but then had a parabolic rise (something like 50% in a year). This is the transition from a boom to a manic phase – driven by extreme investor behaviour rather than fundamentals.

There was a well established mania by the Summer of 1987.

The stock market is itself a measure of confidence – the problem is knowing when this confidence goes too far, too fast.

What we did (and still do) is measure the gap between the stock market index today and its long term trend (being the 200 day moving average). When the index is 15% above the long term trend it is ringing a loud bell, and the higher it goes the louder the ringing! In simple terms this tells us that the market has gone up too far too fast.

By April 1987 the FTSE 100 index was 15% above its long term trend, and by August it was an extraordinary 30% above. This simple, and effective, measure on its own made us very concerned. We had clearly entered a very dangerous phase.

Interestingly, as we saw earlier, stock markets were not particularly over-valued when judged against company profits. So there was no classic investment bubble with a mix of extreme investor behaviour and extreme valuations.

First and foremost this was a behavioural bubble – a bubble in confidence. Not just any old confidence – but that of a crowd, the very powerful investing herd. To most investors there was seemingly unstoppable momentum.

“Madness is rare in individuals, but in groups, parties and nations, it is the rule” (Nietzsche)

TO BE CONTINUED

(First posted 15/09/17)